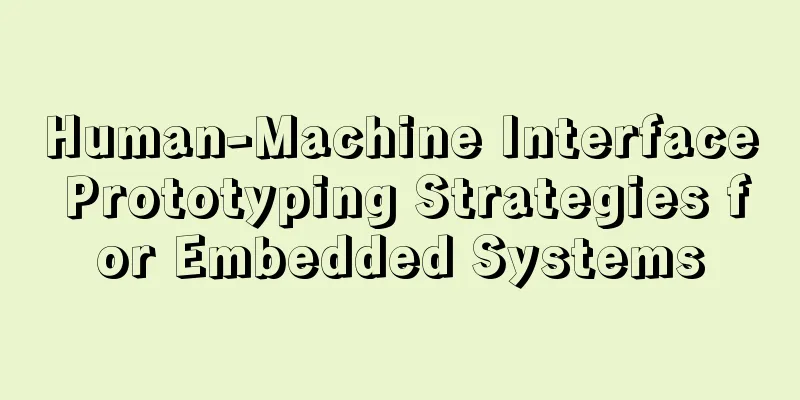

In the past two years, affected by the COVID-19 pandemic and multiple political and economic factors, passenger vehicle production and sales have declined slightly. However, as the global situation enters a new normal, my country's auto market has shown a "recovery" trend. Data from the my country Association of Automobile Manufacturers shows that in the first three quarters of 2021, a total of 14.658 million passenger vehicles were produced, an increase of 10.7% year-on-year.

With the continuous increase in the number of passenger vehicles, vehicle use has put significant pressure on energy supply and carbon emission control. To alleviate this pressure, two common measures are currently being adopted: first, continuously reducing energy consumption per vehicle and improving the energy efficiency of automobiles; and second, using fuels with lower emissions or even zero emissions, currently primarily electricity.

my country's passenger vehicle production trends over the years

Since my country implemented fuel consumption limits for passenger vehicles in 2005, energy-saving targets for passenger vehicles have become increasingly stringent, playing a significant role in promoting carbon reduction in the passenger vehicle industry. Simultaneously, with the development of technologies such as electric vehicles and fuel cell lithium-ion battery vehicles, zero-emission vehicles are playing an increasingly important role in the low-carbon development of the passenger vehicle sector. The "dual-credit policy" introduced in 2017 has become another driving force for the low-carbon development of my country's passenger vehicle industry.

The "dual-credit policy" aims to improve the energy-saving technology of traditional passenger vehicles and promote the development of new energy vehicles. For the former, a key metric is the company's average fuel consumption (CAFC), which is the weighted average of the fuel consumption and production volume of all models produced by a company for a particular model within a year. For the latter, a key constraint is the proportion of new energy vehicle (NEV) credits, requiring companies with an annual production of more than 30,000 traditional vehicles to meet the annual NEV credit target.

The targets for the proportion of new energy vehicle credits and incentives for energy-saving vehicles under the "dual-credit policy" need to be formulated in conjunction with market development, and the current policy cycle is relatively short. As of the end of 2020, the dual-credit management phase of 2018-2020 has been completed, and 2021-2023 can be regarded as the second phase of dual-credit management.

Phase One: A Happy Ending for Everyone or a Mixed Bag of Joy and Sorrow?

In terms of implementation results, the two goals were not actually achieved to the same extent at this stage.

(1) Since 2016, the CAFC value has been declining steadily and slowly. In 2020, it rebounded to 5.61L/100km, failing to achieve the overall target for 2020.

With stricter CAFC (Carbon Fuel Consumption) standards and a reduction in production incentives for new energy vehicles, the decline in CAFC values has narrowed. Joint ventures saw the largest overall decrease, while imported vehicles experienced the smallest. From 2016 to 2019, the average CAFC value of the passenger vehicle industry continued to decline, with an average annual decrease of 4.7%. In 2020, the average CAFC value of the passenger vehicle industry actually increased year-on-year, returning to 5.61L/100km, still significantly below the 5.0L/100km target mentioned in the "Medium and Long-Term Development Plan for the Automotive Industry." Specifically, the average CAFC value of joint ventures declined continuously from 2016 to 2020, with an overall decrease of 14%. The average CAFC value of domestic companies declined the fastest between 2016 and 2019, but due to a rebound in traditional vehicle fuel consumption, a decrease in new energy vehicle production, and a reduction in production incentives, the CAFC value rebounded by 14% year-on-year in 2020, approaching the 2017 level. The overall CAFC value decrease for imported vehicles was only 6.8%.

New energy vehicles have a clear advantage in CAFC (Consumer Cost of Living) accounting. In the Phase IV (2016-2020) fuel consumption evaluation system for passenger vehicles, existing production discounts are applied to new energy vehicles, but their electricity consumption is not included in the calculation. This significantly lowers the CAFC value for companies, especially for domestic brands. Since 2016, the average fuel consumption reduction for traditional vehicles in the industry has been only 1.6%, approximately one-third of the actual CAFC reduction. Domestic brands have seen an average fuel consumption reduction of only 0.4% for traditional vehicles, ranking last among all company types.

The trend of average fuel consumption of passenger vehicles: the blue line represents the CAFC value, and the gray line represents the fuel consumption of conventional vehicles.

The rebound in the industry's CAFC value in 2020 was largely due to the fact that the production multiple of new energy vehicles decreased from 3 times in 2019 to 2 times, while the average fuel consumption of traditional vehicles remained essentially stagnant. In other words, the significant decrease in CAFC value in the early stages of Phase IV was actually just a "numerical" decrease. The seemingly impressive decline in CAFC value, achieved through production multiples of 3-5 times for new energy vehicles, did not effectively improve the energy efficiency of traditional vehicles. On the contrary, the numerous incentives for new energy vehicles weakened the incentive to improve the energy efficiency of traditional vehicles, leading companies to excessively pursue the rapid launch of new energy vehicle projects and concentrate most of their funds and manpower on new energy vehicles, which could easily result in neglecting other aspects.

(2) On the other hand, the new energy passenger vehicle market is booming and the new energy vehicle credit industry has a high compliance rate, but the development among companies is uneven. Domestic brand companies have obvious advantages, while traditional joint venture car companies have difficulty meeting the standards.

The participation of new energy passenger vehicle companies is becoming increasingly active, with penetration rates increasing year by year. In terms of production, the output of new energy passenger vehicles reached 1.205 million units in 2020, an increase of 260% compared to 2016. In terms of production distribution, the production share of joint ventures and wholly foreign-owned enterprises is gradually increasing, and domestic brands are no longer the dominant force. In 2020, the production ratio of new energy passenger vehicles from domestic, joint venture, and wholly foreign-owned enterprises was approximately 6:3:1. In terms of new energy vehicle penetration rate, it reached 6.1% in 2020, an increase of 344% compared to 2016.

During this period, achieving the new energy vehicle credit target was not difficult, but the polarization was severe: domestic brands were the biggest winners, while joint ventures lagged behind. In 2019 and 2020, the industry's new energy vehicle credit ratio was 2.7 and 2.4 times the target requirement, respectively. Overall, the pressure to meet the target was not high, but there was a severe polarization: (1) Domestic brands occupied the high ground in new energy vehicle credits, with an average credit ratio of 64% in 2020, while the ratio of joint ventures was only 9%; (2) Positive new energy vehicle credits were mainly concentrated in domestic brands, with about 90% of domestic brands achieving positive credits in 2019 and previous years. At the same time, joint ventures had more than 80% of their new energy vehicle credits being negative. However, it should also be noted that with the launch of new energy vehicle products by joint ventures and the sales of domestically produced TSLA, the market share of domestic brands' new energy vehicles is being eroded, resulting in a year-on-year decrease in the credit ratio of domestic brands in 2020, while the credit ratio of joint ventures steadily increased.

New energy vehicle credit ratio trend

Undeniably, the "dual-credit policy" has had a significant positive impact on the development of new energy passenger vehicles. For companies primarily focused on new energy vehicles, they can achieve a reduction in CAFC (Common Carrying Capacity) values through new energy vehicles, realizing a double harvest of fuel efficiency and new energy vehicle credits. They may even be able to meet the limits without needing to improve the fuel consumption of traditional vehicles, demonstrating the clear "feedback" effect of new energy vehicles. Simultaneously, traditional energy-saving technologies, which involve high costs and technological barriers, seem to have a greater chance of success when switched to new energy vehicles. This was a key strategy for most domestic brands in the first phase of the "dual-credit policy." With the rapid expansion of the new energy vehicle market, joint venture automakers have also had to increase their investment in new energy vehicles, leading to increasingly fierce competition. However, this will also promote the continuous market penetration of high-quality vehicles, thereby achieving the policy goal of promoting the adoption of new energy vehicles.

In conclusion, although the implementation of the "dual-credit policy" at this stage was a process of "crossing the river by feeling the stones," it has yielded valuable relevant experiences and lessons, and in the long run, it may not be a bad thing.

In the second phase, can we achieve a "two-pronged approach" of energy conservation and new energy technologies?

Despite the ongoing pandemic and the constantly evolving international political and economic landscape, the global commitment to addressing climate change remains unwavering. At the national level, major emitters such as my country and India have successively proposed carbon peaking and carbon neutrality targets. At the regional level, some developed regions are continuously proposing zero-emission action plans and methods for the transportation sector, such as California's Advanced Clean Trucks Ordinance. Based on the experience gained from implementing policies during the 2018-2020 phase, a revised version of the "dual-credit policy" has been released, forming the basis for the second phase of management towards 2023. With the implementation of several policies favorable to energy-saving technologies and vehicles, the passenger vehicle industry is expected to achieve a "two-pronged approach" of energy conservation and new energy technologies in its carbon emission reduction efforts.

(1) The development momentum of new energy vehicles remains strong, and joint ventures have further stabilized the market by increasing their investment.

In the first three quarters of 2021, my country's cumulative production and sales of new energy passenger vehicles approached 2 million units, with a market penetration rate of 13.3% from January to September. Compared to the stagnant growth since 2018, the new energy passenger vehicle market experienced another surge in 2021. On the one hand, after several years of development, the new energy passenger vehicle market has shifted from policy-driven to market and consumer-driven, with continuously improving product quality, increasing choices, and growing consumer acceptance. On the other hand, the global auto market has been widely affected by the "chip shortage," with a particularly significant impact on traditional automobiles. Some automakers have even been forced to halt production, and the demand for certain vehicles has shifted from traditional gasoline vehicles to new energy vehicles.

Trends in the production and penetration rate of new energy passenger vehicles

Domestic brands still hold a significant advantage in the new energy passenger vehicle sector, while joint venture brands and companies like TSLA are catching up. Since the Shanghai Gigafactory went into operation, TSLA's vehicle deliveries in my country have increased rapidly. In 2020, thanks to the strong sales performance of the Model 3, it captured 12% of the Chinese new energy passenger vehicle market. In the first three quarters of 2021, sales of the Model 3 and Model Y in China exceeded 200,000 units, firmly securing a place among the top three in the sales rankings of new energy vehicles in my country during the same period. While joint ventures seem to be struggling to adapt to the Chinese new energy vehicle market due to strategic and product planning factors, their electrification ratio is gradually increasing due to global electrification strategies and mandatory requirements such as the "dual-credit policy."

It's worth noting that among the top ten best-selling new energy passenger vehicles in the first three quarters of 2021, A00-class models, represented by the MINI, contributed approximately 20% of sales, maintaining the "dumbbell" shaped distribution structure of the new energy passenger vehicle market. However, the future demand and potential of the A00-class market are highly uncertain, and some industry insiders believe the boom in the A00-class new energy vehicle market will not last long. Meanwhile, mainstream joint venture new energy vehicle models will primarily focus on the A and B-class markets, intensifying product competition in these segments. In the long run, this will help improve the diversity of new energy products and further stabilize the overall new energy vehicle market.

Distribution of domestic new energy passenger vehicle companies

(2) With the combination of external technical standards and multiple favorable policies, energy-saving technologies are expected to see concentrated development.

As mentioned earlier, the wave of electrification is sweeping in, and traditional energy-saving technologies must seize this last opportunity for development. The experience gained from the previous "dual-credit policy" has also presented policymakers with a challenge: how to balance energy conservation and new energy technologies?

In fact, considering the complexity of my country's geographical environment and energy distribution, the "Energy-Saving and New Energy Vehicle Technology Roadmap (2.0)" has set high expectations for energy-saving vehicles, mainly hybrid vehicles: at least half of traditional passenger car sales after 2025 will be hybrid vehicles, and relevant experts also advocate against setting a "ban on combustion engine vehicles" timetable. However, to achieve this goal, certain preferential policies are necessary in practice. The first-stage "dual-credit policy" gave excessively high production discounts to new energy vehicles without considering electricity consumption, and set low technical thresholds for new energy vehicle product parameters, causing most companies to switch to the new energy vehicle market to obtain "quick and easy" economic benefits. Although the fourth-stage fuel consumption limit standard for passenger cars also gives production discounts to energy-saving vehicles with fuel consumption below 3.2L/100km, the discount is lower than that for new energy vehicles and the threshold is higher, resulting in poor implementation.

Based on the experience gained from the implementation of the "dual-credit policy" from 2018 to 2020, the production or import volume of low-fuel-consumption passenger vehicles will be discounted during the 2021-2023 period. At the same time, the company's average fuel consumption of traditional energy passenger vehicles will be a prerequisite for the carry-forward of its new energy vehicle credits.

Furthermore, in October 2021, the national standard "Evaluation Method for Energy-Saving Effects of Passenger Vehicle External Cycle Technologies/Devices" (Parts 2, 3, and 4) was officially published, evaluating and affirming the external cycle energy-saving effects of idle start-stop, air conditioning, and brake energy recovery systems. In fact, in the 2020 CAFC calculation for passenger vehicle companies, the Ministry of Industry and Information Technology had already pointed out that "for vehicles using one or more external cycle technologies/devices, their fuel consumption can be reduced accordingly by a certain amount," and taking into account factors such as technological maturity and fuel-saving level, it granted fuel consumption reductions of 0.15 liters, 0.1 liters, and 0.15 liters per 100 kilometers (0.05 liters for 12V) for vehicles using external cycle technologies such as idle start-stop, shift reminder, and brake energy recovery.

Data shows that hybrid passenger vehicles have shown a strong upward trend in the past two years, and their market penetration rate has continued to increase. However, Japanese brands still dominate the domestic hybrid passenger vehicle market, with Toyota and Honda sharing the market share.

HEV passenger vehicle sales and market penetration

What is the future of the "dual-credit policy"?

my country's targets and expectations for the overall average fuel consumption of passenger vehicles have shown good consistency. "Made in my country 2025" set a target of reducing the overall fuel consumption of new passenger vehicles to around 4 liters per 100 kilometers by 2025. Furthermore, the fuel consumption limit standards for passenger vehicles have been implemented since 2005, and corporate average fuel consumption management has undergone nearly a decade of development. These measures have effectively ensured the downward trend in the overall fuel consumption of passenger vehicles.

Compared to fuel consumption management, the new energy vehicle credit policy within the "dual-credit policy" is relatively new and more susceptible to market changes. As new energy vehicles further develop, the formulation of its targets and the weighing of its advantages and disadvantages become more complex. The new energy vehicle credit mechanism largely references California's zero-emission vehicle (ZEV) credit trading mechanism. Although the latter has undergone decades of development and evolution, it seems somewhat outdated in today's rapidly evolving electrification landscape.

In California, prior to 2017, ZEV credits were primarily composed of credits from vehicles other than "pure electric vehicles." However, since 2017, the main body of ZEV credits has rapidly shifted towards pure electric vehicles. During this period, ZEV credit trading also underwent significant changes: with the development of zero-emission vehicle technology, the California Air Resources Board (CARB) raised the minimum ratio of ZEV credits and the minimum ratio of completely zero-emission vehicles, leading to a significant increase in credit trading volume after 2010, especially between 2012 and 2015, when traded ZEV credits accounted for over 10% of the total credits. Subsequently, with major automakers' R&D and market investment in zero-emission vehicle technology, more and more automakers began to emerge and accumulate more and more ZEV credits, causing credit trading volume to decline rapidly. For example, in the 2019-2020 trading cycle, major California automakers had considerable accumulated ZEV credits. Toyota's accumulated ZEV credits were close to 210,000, second only to TSLA, and GM's credits exceeded 150,000. Conversely, only 6,000 credits participated in trading during this cycle.

Trends in total California ZEV credits and the percentage of credits traded.

Not only in California, but also in the other 11 ZEV states, credit trading shows a similar trend. On the one hand, because the types of vehicles eligible for credits are diverse, most large automakers can meet the target requirements through diverse product strategies. On the other hand, ZEV credits do not expire and accumulate annually within the company, making them less susceptible to fluctuations. However, this also indicates that the binding force of the ZEV credit target appears to be weakening. Based on the 2025 ZEV credit ratio of 22%, the market penetration rate of zero-emission vehicles will be approximately 8%, a target that currently seems quite outdated.

To better facilitate the use of the ZEV mechanism, CARB is preparing and ready to release new policy tools targeting 2035. Where applicable, the 2035 goal is to achieve 100% ZEV transformation.

While my country's situation differs from the US, there are some similarities. Overall, the new energy vehicle credit targets are already lagging significantly, but there are huge differences in the production and sales ratios of new energy vehicles among companies. At least in recent years, it has become very difficult for mainstream joint ventures to meet their existing credit targets through the sale of new energy vehicles themselves. 2021 was widely hailed by the media as the "marketization year" for new energy vehicles. Due to a combination of factors, the penetration rate of new energy passenger vehicles has continued to rise. As a mandatory policy tool, what compliance targets will the "dual-credit policy" set in the future? How will it be managed? At the same time, with the continuous increase in the volume of new energy vehicles, when and how will upstream greenhouse gas emissions from the power industry be included in the "dual-credit policy"? These are all questions that relevant departments should consider.